Online showing schedulers have become standard in real estate. Tools like ShowingTime and similar platforms make it incredibly easy for agents to book showings, coordinate availability, and avoid the endless back-and-forth of phone calls and texts. From a logistical standpoint, they’re efficient. They save time. They reduce friction. And they help listings get shown faster.

Online showing schedulers have become standard in real estate. Tools like ShowingTime and similar platforms make it incredibly easy for agents to book showings, coordinate availability, and avoid the endless back-and-forth of phone calls and texts. From a logistical standpoint, they’re efficient. They save time. They reduce friction. And they help listings get shown faster.

But there’s another side to this that often goes overlooked.

These platforms don’t just help agents schedule showings. In many cases, they also quietly reveal something else: demand.

And demand—or the lack of it—is one of the most powerful negotiation tools in real estate.

What Buyers’ Agents Can See

When a showing calendar is visible—even partially—to agents scheduling appointments, it can provide insight beyond just availability. It can tell a story.

If a calendar is filled with blocked time slots, overlapping showings, and limited availability, that signals interest. It suggests competition. It creates urgency.

But when a calendar is wide open for days—or even a full week—that sends a very different message.

It suggests the property may not be seeing much activity.

And that changes how buyers and their agents approach negotiations.

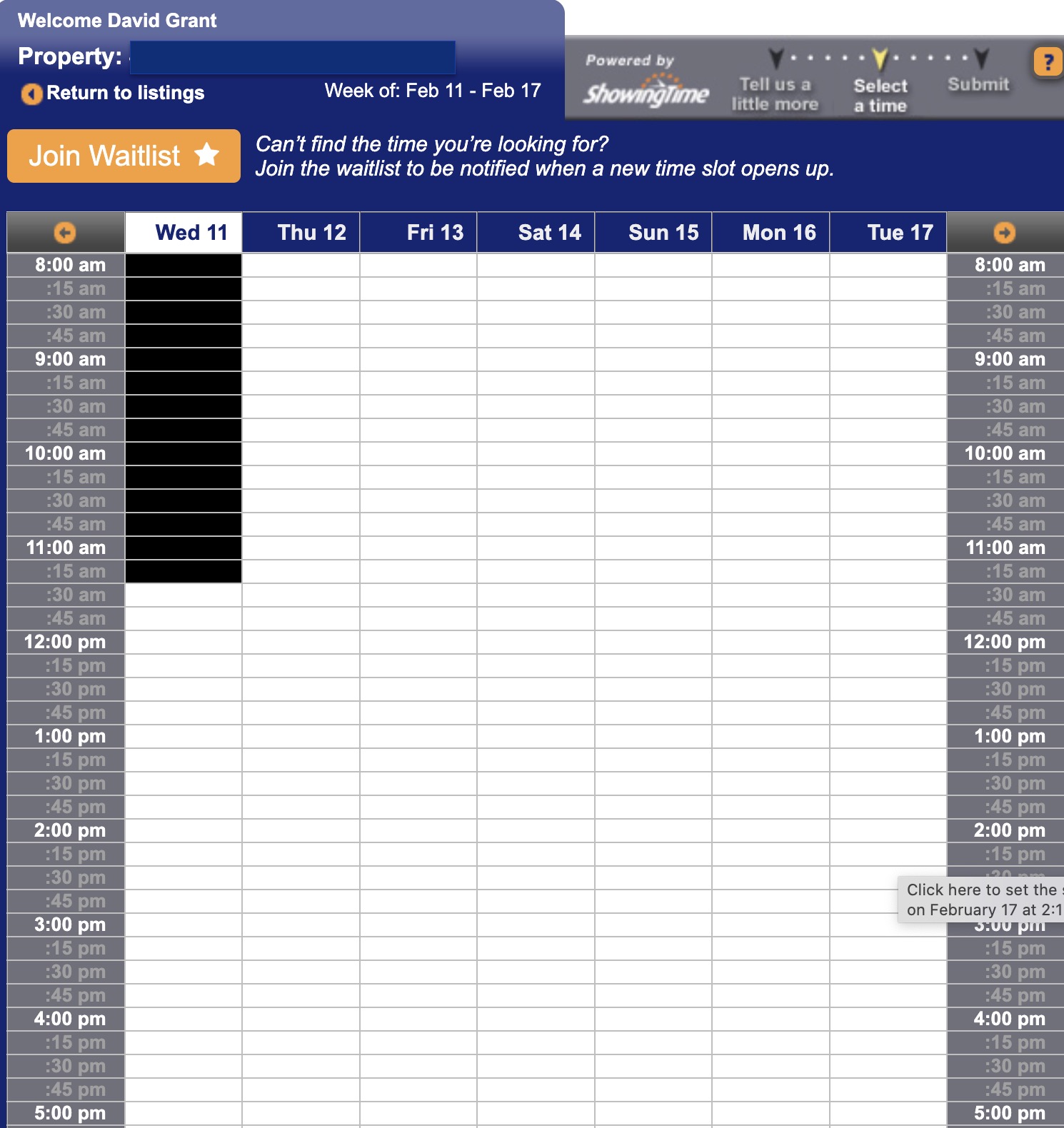

A Real-World Example

I’m currently negotiating on a property for a buyer where the showing calendar is completely open for the next week. There are no showings scheduled. No blocked time slots. No indication of any upcoming activity.

As a buyer’s agent, that information is incredibly valuable.

It tells me:

-

There’s likely no immediate competition.

-

The seller may not have strong leverage at the moment.

-

There’s no urgency to rush or escalate the offer.

-

The buyer may have room to negotiate more aggressively.

This isn’t speculation. It’s simply reading the available data.

If the calendar were full, the strategy would be different. But when it’s empty, it naturally shifts the negotiating position.

Why This Matters for Sellers

Many sellers assume showing activity is private. They believe only their agent knows how much interest their property is receiving.

But in reality, online scheduling tools can indirectly share that information with every agent who attempts to schedule a showing.

That may not matter in the first few days of a listing, when activity is typically strongest. In fact, a busy calendar can actually help reinforce demand and encourage stronger offers.

But if a listing has been on the market for a few weeks and the calendar is empty, that visibility can weaken the seller’s negotiating position.

It gives buyers confidence to push harder.

It removes urgency.

And urgency is often what drives stronger offers.

Convenience vs. Strategy

There’s no question that online scheduling tools are incredibly useful. They make the process smoother for agents, sellers, and buyers alike.

But convenience doesn’t always align perfectly with strategy.

From a listing perspective, controlling the perception of demand is important. Real estate is not just about the physical property—it’s also about positioning.

Perception influences behavior.

Behavior influences offers.

A More Strategic Approach

This doesn’t mean online scheduling tools shouldn’t be used. They absolutely should. But how they’re used matters.

Some more strategic approaches include:

Using approval-based scheduling

Instead of fully open calendars, require confirmation before showings are finalized.

Creating defined showing windows

Group showings into specific time blocks rather than leaving every slot open all week.

Avoiding overly transparent availability

Limiting how much agents can see about open or unused time slots helps maintain negotiating neutrality.

Managing early momentum carefully

The first 7–14 days are critical. Strong early activity creates long-term leverage.

What This Means for Buyers and Sellers

For buyers, tools like this provide insight that can help guide negotiation strategy. It allows them to make informed decisions about timing, pricing, and leverage.

For sellers, it’s a reminder that every part of the listing process—including scheduling—plays a role in positioning the property.

Marketing isn’t just photos and pricing. It’s also about managing information.

The Bottom Line

Online showing schedulers are here to stay, and they provide real benefits. They make the showing process easier, faster, and more organized.

But they also quietly reveal signals about demand.

And in real estate, demand—or the perception of demand—is everything.

Understanding that dynamic allows agents to better protect their sellers’ negotiating position and allows buyers to make smarter decisions.

Like many tools in real estate, it’s not just about using them.

It’s about using them strategically.

How to Get Your Home Photo-Ready for Listing Day

How to Get Your Home Photo-Ready for Listing Day When Do Homes Come on the Market — and When Do They Actually Sell?

When Do Homes Come on the Market — and When Do They Actually Sell? Here is a lesson that I learn every few years....

Here is a lesson that I learn every few years....